I googled this exact question and was disappointed with the content on the first page of results. A third of the results were ads for refinancing, another had click bait titles on reasons for why you should consolidate, and the last few websites talked about why it might not be a good idea, but didn't delve into exactly why. In my frank opinion, the answer to this question is: probably not. To be clear, I'm talking about loan consolidation, not loan refinancing - which is a completely different subject. Loan consolidation, especially in today's student loans are nothing more than a weighted average of your interest rate. Take for example the following:

Dr. Hero has an outstanding balance of $100,000 in student loans. The break down of his loans are as follows:

- $60,000 at 4%

- $20,000 at 6 %

- $20,000 at 10%

The weighted average of his loan balance would be:

So by consolidating Dr. Hero would have one large loan at 5.6% instead of having 3 different loans at 3 different rates. This, however, isn't the final rate. On studentaid.ed.gov they specifically state that the interest rate on a consolidated loan is "rounded up to the nearest one-eighth of 1%". So instead of 5.6%, you are actually incurring interest at 5.625%. Ouch! However, that is not the main reason for why you should avoid consolidation.

So by consolidating Dr. Hero would have one large loan at 5.6% instead of having 3 different loans at 3 different rates. This, however, isn't the final rate. On studentaid.ed.gov they specifically state that the interest rate on a consolidated loan is "rounded up to the nearest one-eighth of 1%". So instead of 5.6%, you are actually incurring interest at 5.625%. Ouch! However, that is not the main reason for why you should avoid consolidation.

Fundamentally there is a strong argument AGAINST consolidating your loans, and it isn't a new concept. In finance, there is a general principle that asserts any time you have loans, you want to pay down the highest interest loan first. So lets run through a simulation for student loans.

Dr. Hero puts $6,000 a year away into paying down his debt. He was smart and didn't consolidate his loans and put his payments against the highest interest loan first.

We see that Dr. Hero is able to pay off his balance in 31 years by targeting his high interest loans first. Now, let's say instead of being smart, he fell into the trap and consolidated his loans at 5.625% while paying $6,000 dollars a year against his loan.

OUCH! Dr. Hero is putting away the same amount of his annual income, but now he is stuck with a payment plan that lasts 52 years. The difference is 21 years! The primary reason for this difference is obvious. By paying down the principle of the higher interest loan first, you're reducing the interest that is compounded in the future. There is another, albeit smaller, reason to account for this difference in payment time that I didn't realize until actually doing the calculations.

Student loan interest is simple interest (atleast in IBR programs). Capitalization (when the outstanding interest now becomes part of principle) doesn't occur unless the loan enters repayment, deferment ends, forbearance ends, the loan defaults, the payment plan changes, or consolidation occurs. Simple interest benefits the borrower particularly when the payments on the interest are not fully covered on a loan. That means the loan growth is linear, not exponential (as you can see in the first graph during the which the lower interest loans aren't even being touched). However, when the borrower starts to cover the interest payments on the loan, the curve is no longer linear, but rather an exponential function which means that the benefits of simple interest are not fully utilized during that time. In effect, you are taking advantage of the fact that the growth on your loan balance is linear and mitigating the exponential resistance on payment of your loans while reducing payments on your higher interest loans.

So, then. You should never consolidate your loans, right? Again, probably.

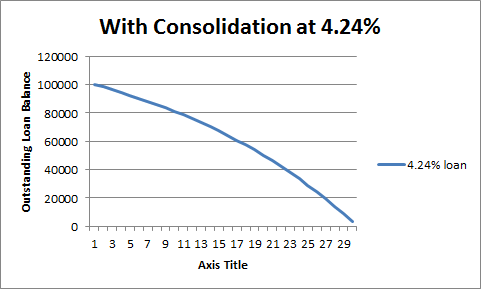

An interesting question would be, at what consolidated interest rate would the government have to give you to match the non-consolidated payment schedule? The answer, after tweaking with the numbers in the scenario where you pay $6,000 a year is 4.24%.

WOW! That's a difference of 1.01% of annual interest that the government is pocketing just because you made the mistake of consolidating. However, that also means that if the government gave you a consolidated loan less than the said interest rate, it is the borrower that benefits. Unfortunately, the government offers no such deal.

Chances are, unless you're given a significant discount for the consolidation rate, don't even bother! My question is then, why does the government even offer consolidation, knowing that it's a bad deal for the borrower? Why offer the trap to students who are supposedly the future of America? If the government were to act in an honest nature, it would offer a fair rate of consolidation, not one that adds more debt to the backs of the future generation which is already burdened with over 3 trillion dollars of student loan debt. On the the next section about Anti-Consolidation.

No comments:

Post a Comment